What Are My Tax Implications if I Sell and Take Long Term Gains Then Buy Same Stock Again?

**The information on this web page is provided for informational purposes only and should not be considered as legal, tax, financial or investment advice. Since each individual's situation is unique, a qualified professional person should exist consulted earlier making financial decisions.**

From the following article you will learn about the tax treatment of selling commercial real manor in the Us and ways to legally reduce your tax liabilities. We will discuss:

- long and short term Federal capital gains tax, its rates, and when it's applied or non practical

- state income tax

- majuscule loss and how to apply information technology to reduce your taxation liability

- depreciation recapture

- 9 legal ways to reduce your tax liability.

Note: you might likewise exist interested in our guides on commercial real estate property revenue enhancement:

- ABC's of Commercial and Industrial Existent Estate Belongings Taxation

- 5 Robust Commercial Belongings Taxation Reduction Methods

Read on to larn more near proper tax planning on the sale of commercial property.

Tax Treatment of Selling a Commercial Investment Property

Federal Capital Gains Tax (CGT)

What Are Capital Gains?

Let's not make this harder than information technology already is. Generally, capital gains are profits from investments sold for more original buy prices. They are called realized capital gains. However, when it comes to commercial real estate investment property, there'south a twist.

Unlike stocks with stock-still purchase prices, original real estate prices are adapted for taxation purposes. On acquisition, a tax or cost footing (including legal fees, transfer taxes, and other endmost costs) becomes part of the purchase price. Likewise, during buying, an adjusted basis calculation often includes capital improvements (east.one thousand., roof replacements), thereby increasing purchase costs and reducing any capital gains on futurity sales.

What Is Non Considered Majuscule Gains?

Backdrop qualified for capital gains are immovable investment properties — anything considered real estate, such every bit land, buildings, decks and pools. But there is an of import caveat: gain from a sale of business assets aren't considered majuscule gains.

A business asset is a piece of holding or equipment bought primarily for business utilize. They may be depreciated or expensed in the purchase year under Department 179 and eventually written off.

The same is truthful for real manor developers in comparison with real estate investors. Proper classification has been oft litigated. Jennifer Seaton, Partner RSM U.s. LLP, cautions that "Decisions and actions that occur early in the conquering phase of real estate investments can have far-reaching implications for the taxability of real estate investments."

Whatsoever uncertainty about the post-obit five considerations (Seaton, 2014) may portend the need for professional counsel:

- Frequency and continuity of sale.

- Nature and extent of improvements and development activities.

- Solicitation, advertising and sales activities.

- Extent and substantiality of transactions.

- Nature and purpose for belongings property.

Profits from business organization activity are typically treated equally ordinary business income rather than capital gains.

Basic Capital letter Gains Calculation

A simple capital gains calculation looks similar this: adapted gross gain from the auction of a qualified capital asset (say $200,000) minus the adjusted original purchase toll of that property (say $150,000) equals a $50,000 capital gains amount. This formula applies to both short- and long-term capital letter gains. Yes, information technology gets harder from here on but that'south it, a capital gain in a nutshell.

As usual, the devil is in the item. Let's showtime with brusk-term gains, one of the ii major categories. Every bit you will see, taxation rates skyrocket compared to long-term gains.

Short Term Capital Gains (STCG)

Definition and Explanation

Capital letter gains on auction of commercial immovable belongings held for one year or less are classified as curt-term. Again, these gains on real estate sales — such as buildings and land — are calculated past subtracting adapted sales prices from adapted buy prices to compute capital gains.

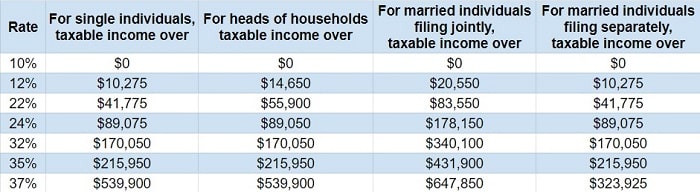

Short Term Capital Gains Tax Rates in 2022

Gains are taxed as ordinary income at the regular individual income revenue enhancement rate. Per the IRS Tax Rate Chart below, Articulation filers with $75,000 in short-term majuscule gains fall into the 12% charge per unit bracket rather than a 0% tax rate shown in the side by side section for long-term capital gains. Clearly, the asset holding flow is pivotal to your commercial existent manor tax planning.

2022 Ordinary Income Revenue enhancement Brackets and Rates

Here is how to start the federal tax calculation.

- If you lot purchased the property, determine the number of days that lapsed between purchase and sale dates.

- If the property was a gift, calculate the number of days betwixt the engagement acquired past the original owner and your sale date.

- If the property was inherited, calculate the number of days between the original possessor's appointment of death and the sale date.

If the number of days from acquisition to sale is 365 or fewer, it'southward a short-term capital proceeds.

Long Term Upper-case letter Gains (LTCG)

Definition and Caption

Gains on the sale of commercial real estate property owned for more than one twelvemonth are classified equally long-term. Calculating these gains is covered in the What Are Capital Gains? section in a higher place. Information technology's no different than the short-term capital gains adding–but for sure–tax rates are much lower. Only subtract the property'due south adjusted cost footing from the auction's adjusted gross proceeds for upper-case letter gains, a.grand.a., profits.

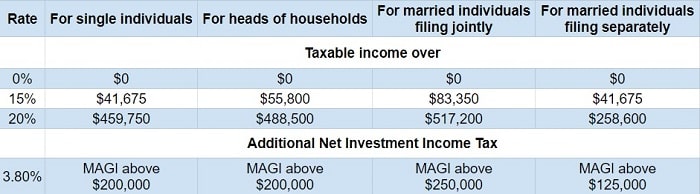

Long Term Capital Gains Revenue enhancement Rates in 2022

Per the IRS nautical chart below, those Joint filers with $50,000 in capital gains now fall into the 0% rather than 12% revenue enhancement bracket for short-term capital gains (chart to a higher place). What a departure a day can brand! No brainer it would seem unless there's a looming financial crunch (a xx% US unemployment rate peradventure?) or other compelling reasons to sell before.

2022 Tax Rates on Long-Term Capital Gains

Annotation also at the bottom of the rate table an Boosted Net Investment Income Revenue enhancement that applies to Modified Adjusted Gross Income (MAGI) over certain thresholds. Information technology'due south a iii.eight% surtax on high earners enjoying investment income revenue enhancement breaks, i.east., deductions, credits, and other tax perks. The surtax applies to most investment sale gains higher up the tabular array's limits ($250,000 for Joint filers).

Capital Loss

Definition and Explanation

Capital losses occur when a qualified result such as the auction of investment property results in a loss. A loss is sustained when the original purchase cost (adjusted for added costs) is greater than the sales price (adjusted for selling expenses).

To qualify as a capital letter loss, the belongings must have been held for investment and not personal utilize. Too, not until sold will losses be recognized. For example, if a commercial real manor investor paid an adjusted $500,000 for rental belongings that sold for an adjusted $475,000 two years later, the investor realized a $25,000 capital loss.

How Upper-case letter Loss Reduces the Capital Gains Taxation Amount

Majuscule gains are netted confronting capital losses every bit outlined in the Brusk Term Uppercase Gains section above. Capital losses offset each tax year'due south new majuscule gains, with any residual (unused) losses carried forward year-to-year until wearied.

What to practice with your capital gains, short and long-term when preparing to file your federal tax render? Showtime, all upper-case letter gains and losses must be deemed for and netted by taking the following steps.

- Decrease any short-term losses (say $0.00) from short-term gains (say $50,000) for $50,000 in short-term net gains.

- Subtract any long-term losses ($0.00) from long-term gains ($50,000) for $fifty,000 in long-term net gains.

- Subtract short-term net losses ($0.00) from long-term net gains ($50,000) for $50,000 in long-term capital gains.

In 2022, for Articulation filers, the $fifty,000 brusk-term capital gain falls under the 12% tax bracket for Ordinary Income (Ordinary income tax Rates chart above) while there'south no tax on the long-term majuscule gains (Long-term capital gains tax Rates chart above).

In addition, another taxation may be imposed on property sold for more than its depreciated value. Called a Depreciation Recapture tax, information technology applies to commercial real manor property. The amount recaptured is taxed at a 25% rate. That calculation is covered subsequently under the Depreciation Recapture department.

Of course, this does not terminate the whole brusque-term capital letter gains story. Federal taxation law is legendary for its endless complexities. Just be sure to take this with you: asset property periods are pivotal to your commercial real estate tax planning.

State Capital Gains and Income Taxes

Many states impose uppercase gains and income taxes. Still, conformity is oft lacking, making country-past-state coverage here impractical. Some states allow taxpayers to deduct Federal income taxation paid from state taxable income. Others apply special rules to capital gains income. Research and consider your local state income taxation rules.

Depreciation Recapture

What Is Depreciation of a Property?

Depreciation is an expense. Each year as depreciable property declines in value, depreciation allows you to tape losses incurred over time, thereby more than closely reflecting true value. Of the 2 commonly used depreciation methods, straight-line produces the same expense each year ($one,000 on 10-year property with a $x,000 purchase footing) while accelerated depreciation forepart-loads the expense.

IRS rules for depreciation include:

- you must own the property.

- information technology must be a business organisation.

- you can't depreciate a property held mostly for personal use.

- it must have a determinable life span exceeding one twelvemonth.

- it cannot be piece of furniture.

How Does Depreciation Recapture Piece of work?

In some instances, both capital gains on depreciable property and recaptured depreciation are taxed. Capital gains are one part of the tax calculation. A second depreciation-related portion is taxed at a higher recapture charge per unit. When an investment holding is sold for more than its depreciated value, a recapture tax of up to 25% applies.

For instance, later on four years your property with a $100,000 cost ground and ten-year lifespan now has an adjusted cost basis of $60,000. It sold for $65,000 and you've subtracted (say $1,000 in selling costs) from the sale toll. At present $64,000 in adjusted sale gain are subtracted from the $lx,000 sale value for $4,000 in depreciation recapture. The IRS volition care for this recapture equally ordinary income.

If there was a loss when the depreciable property sold, at that place'southward no depreciation recapture. Besides, the IRS will compare the asset's realized proceeds with its depreciation expense. The smaller figure is determined to be the depreciation recapture amount.

Instance of Computing the Capital Gains Tax on Commercial Belongings

Equally an investment rather than business activity, permit's take commercial rental property bought for $550,000 in May 2010 and sold 10 years later for $400,000. The land was appraised at $75,000 with recordation, legal fees, transfer taxation, et al, costing $25,000. This sets the building's adjusted cost basis at $500,000 ($550,000 paid minus the land valued at $75,000, plus $25,000 in acquisition costs). At present a $100,000 majuscule loss may kickoff any capital gains in that year. Besides, a $iii,000 maximum may starting time ordinary income with whatever residual carried frontward only, never to dorsum-years.

Nonetheless, a depreciation recapture revenue enhancement is due. The IRS' depreciation period is 39 years on commercial rental property. Rounded accumulated depreciation totals $128,210 after 10 years ($500,000 divided by 39 = $12,821 ten 10 years), setting the holding's depreciated value at $371,790 ($500,000 minus $128,210) on the sale date. This means you pay a 25% recapture tax on $28,210 ($400,000 sales price minus the $371,790 depreciated value).

Transfer Tax

All but thirteen states and some localities impose the transfer tax, either on the buyer or seller. It is assessed on real property when ownership of the holding is exchanged betwixt parties and is included in the closing costs paid during the commercial property transaction.

How to File Taxes After the Sale

For class 1040 filers, ordinary income from investment holding sales is reported on Grade 8949 and Schedule D along with filing capital gains taxes.

Income from sales of assets used by dealers in their trade or business are reported on Course 4797, including the depreciation recapture taxation.

The nine states listed above have no income tax. Most states with the tax generally conform with IRS' definitions and treatments.

9 Ways to Avoid or Minimize Capital Gains Revenue enhancement on Selling a Commercial Investment Property

In this department we will give you a bones understanding of what methods of reducing your capital gains revenue enhancement obligations exist. To learn about how they piece of work in more detail, read our guide 9 Ways to Avoid or Minimize Uppercase Gains Tax on Commercial Real Estate.

#i Deduct Uppercase Losses

Until wearied, upper-case letter losses offset uppercase gains. For example:

- In 2016, your $xl,000 capital loss offsets a $14,000 proceeds, along with a $3,000 offset of ordinary income.

- With no upper-case letter gains the following two years, $six,000 offsets ordinary income.

- In 2019, $10,000 in majuscule gains and $3,000 in ordinary income are offset.

- Now $4,000 in capital losses are left for future use.

#2 1031 Tax-Deferred Exchange

In like-kind belongings exchange, investors may defer paying capital gains, depreciation recapture, and income taxes on investment real manor property when it's sold solely to reinvest the gain in some other investment property.

Near oft these exchanges are delayed (Starker or forrad substitution), requiring sale proceeds be held past qualified intermediaries until reinvesting them in some other property. There are also opposite exchanges (replacement belongings is acquired earlier the relinquished property is sold) and simultaneous exchanges (investors swap each other's properties at the same closing, no qualified intermediary required).

Flipped belongings doesn't qualify for a 1031 commutation. Any cash received to compensate the property value difference (boot) is taxed. In that location are other many important rules for this type of transaction to be valid.

If you lot are considering a 1031 exchange, accept a look at our directory of pinnacle-rated 1031 exchange companies (qualified intermediaries) serving your surface area.

#iii 1033 Tax-Deferred Exchange

Much like Department 1031, realized gain from an involuntary conversion (eastward.m., loss to casualty or condemnation) tin be deferred if the owner acquires similar replacement property.

However, some Section 1031 restrictions don't apply: no 45-day deadline for identifying a replacement; insurance proceeds need not be held until the replacement property is acquired; and no qualified intermediary (QI) is required.

#4 Section 721 Tax-Deferred Commutation

A Section 721 Exchange or UPREIT allows investors to substitution investment property for Real Manor Investment Trust (REIT) shares or an Operating Partnership without triggering a taxable consequence.

No replacement holding is required, and sale proceeds may accept already been given to the REIT. As with Sections 1031 and 1033, investors' goals typically include tax deferral, diversification, and estate planning.

#5 Department 453: Installment Sale Tax Deferral

Under Department 453, taxation deferrals are permitted in one of these cases:

- when accepting a bear back promissory or installment note on disposition. As a seller yous defer capital gains income tax recognition until principal payments are received.

- periodic annuity payments are received. Deferred upper-case letter gains amounts are recognized pro rata on principal payments as received.

Of import: depreciation recapture is not deferred.

#6 Opportunity Zones

Selected by land governors in 2018, Qualified Opportunity Zones (QOZs) were created in all fifty states and half dozen territories to revitalize economically distressed communities. Incentives included allowing income taxes on reinvested capital gains proceeds to be deferred and reduced. Held for 10 years, a permanent income tax exclusion applies to capital gains earned postal service-investment; depreciation recaptures go untaxed; and 15% of the original gain goes untaxed after 7 years.

#7 Hold the Holding for More than than a Yr

Called long-term, such properties may qualify for significant capital gains tax benefits (encounter the What Are Capital letter Gains? department of this guide). If then, existent estate sale profits are taxed at long-term rates starting at $xl,000 applied at 0%, 15% or 20% rates depending upon your taxable income and filing status. Conversely, short-term rates kickoff at $x,000 and tops out at 37%.

#8 Charitable Remainder Trusts

Appreciated avails may be transferred to Charitable Remainder Trusts (CRT) taxation costless for a specific term. Since CRTs are tax-exempt, the trustee (or yourself as trustee) may sell these assets, thereby allowing proceeds to compound taxation gratis.

All the while you receive periodic distributions, initially as ordinary income. Despite that when the trust ends, x% stays with it and is used for charity, tax savings often dwarf that loss.

#9 Retirement Plans with Revenue enhancement Advantages

Traditional plans include:

- Annuities — simply the earnings portion of this income stream is taxed.

- IRAs and 401(k) — tax on contributions are deferred while distributions later 59½ are taxed as ordinary income.

- Roth IRA — when held 5+ years, there's no tax on withdrawals later on 59½.

- Non-retirement brokerage accounts — investments with long-term gains taxed at low rates on distribution.

Source: https://propertycashin.com/resources/tax-on-sale-of-commercial-property/

Belum ada Komentar untuk "What Are My Tax Implications if I Sell and Take Long Term Gains Then Buy Same Stock Again?"

Posting Komentar